Should I Increase my 401(k) Contribution?

It has certainly been a different year for all of us.

The COVID-19 pandemic we are experiencing has impacted countries, governments, businesses and markets. Many Americans also looking at the impact of COVID-19 on their 401(k) retirement savings.

History has always shown that we will rebound, as our resiliency is second only to our resolve.

We are born with an innate ability to find opportunity where challenges exist. Now, we should consider a proactive measure instead of embracing fear and doubt. That way, when we come out of this pandemic, we are positioned to be ahead of the curve. After all, the market has always experienced peaks and valleys, and history dictates that the market will recover.

Every market crash we have ever been through has been followed by not just growth but extreme growth.

While it might be time to bunker up and isolate yourself for health reasons it is not a time to bunker your investing power. Anyone with an acumen to investing will tell you that during times of peaks you sell, and when the market is in a perceived valley you buy. For those Americans fortunate enough whose job and/or income has not been adversely affected by this pandemic, now is not only the time to continue to make 401(k) contributions, but to consider increasing one’s 401(k) contributions.

By participating in a 401(k) plan savers are able to take advantage of the theory known as “dollar cost averaging” which is “an investment strategy in which an investor divides up the total amount to be invested across periodic purchases of a target asset in an effort to reduce the impact of volatility on the overall purchase.” (Investopedia, 2002) Seizing an opportunity to buy more shares of mutual funds at a fraction of the cost is indeed an opportunity to get ahead and achieve protection for retiring comfortably. With most market indices down over 30% as of March 23rd, a recurring payroll contribution to an all equity mutual fund will purchase 30% more shares than it would have just a couple of months ago. When the market goes up, a plan participant will have more shares to appreciate.

We experienced a historical 11-year bull market, so a bear market was inevitable.

During this time, low-cost 401(k) index funds became the preferred investment. You will need to adopt a granite-like firmness of purpose to continue to not only be in the market, but also continue purchasing equities, and not be deterred by their recent steep decline.

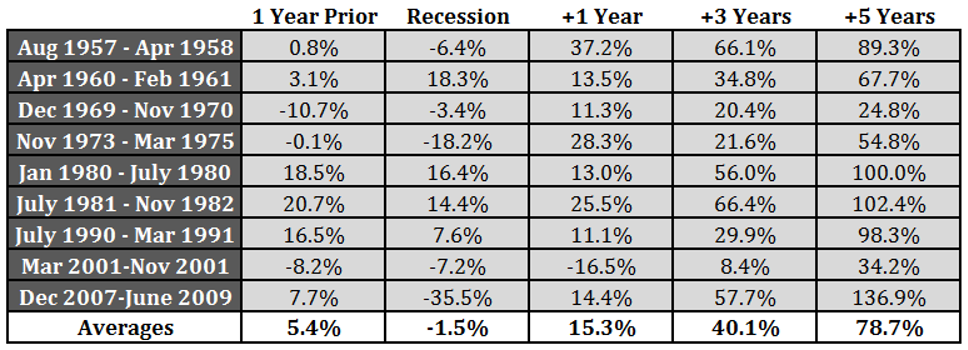

We can see the payoff by looking at recent history. If a participant had continued to buy shares of stock mutual funds during our last recession -- not only would your short-term losses have been recovered, those shares purchased during the 2008 experienced aggressive growth. As seen in the table below from A Wealth of Common Sense, the 2008 recession manifested itself by yielding a 35.5% loss in the market. However, the resilient nature of the S&P 500 yielded growth to the tune of 14.4% in year one, 57.7% in year three and 136.9% by year five post-recession.

If you sold, yes, you got out of the market and shielded yourself from additional losses, but you could have made all your money back with a profit by staying invested in the market and increasing your contributions.

What if, instead of selling or stopping your contributions, you bought more shares at a fraction of the cost?

Where would your portfolio be — or better yet — knowing what you know now, where will it be? For any participant with the financial means, there is an argument to strongly consider increasing contributions and staying the course.

Your future self will thank you.

A quick thought to share for those of you in retirement or ready to enter retirement shortly.

Stave off the impulse to sell your entire portfolio. If you do need to sustain living standards, consider utilizing your cash positions first, bonds secondly, and do your best to wait out the market’s recovery.

Give some thought to delaying your retirement.

As it pertains to your equity positions, sell just what is needed to survive after your cash has been depleted and delay an overall sell off. Your account will recover. No bear market has lasted longer than two years.