Why Choose a Safe Harbor 401(k) Plan?

Offering a small business 401(k) benefits package is a normality today. It not only shows attention to your employees’ future, but also attracts top talent for future projected growth and stability. When I’m speaking with an interested business owner, the first question that usually comes up is: Will I need to offer an employer contribution? The answer is “no” ...but it’s worth considering.

Continue reading to learn more about Safe Harbor 401(k) rules and 401(k) plans.

A Safe Harbor 401(k) Plan is a type of 401(k) Plan with a mandatory employer contribution that allows the plan to satisfy annual compliance tests. The plan will automatically pass ADP and ACP Nondiscrimination Tests and will be deemed as satisfying Top Heavy minimum contribution requirements. This plan design allows highly compensated and key employees maximize their personal deferral contributions ($19,500) for 2020. If you do not offer a Safe Harbor employer contribution, your plan is subject to these tests, and there may be limitations to deferral contributions for key and highly compensated employees.

Let’s Define “Key Employees”

The IRS Guidelines define “key employees” as any of the following:

Officers of the company with gross compensation in excess of $185,000 for 2020

Individuals who own 5% or more of the company in the current or previous year

Individuals who own 1% of the company whose annual pay is more than $150,000

If you meet any of those criteria and want to maximize your contributions, your 401(k) plan will most likely need to be within Safe Harbor provisions. As I noted earlier, it does require a mandatory employer contribution. The three options for mandatory employer contribution are:

Basic Match

$1 for $1 on the first 3%, $0.50 on the $1 on the following 2%

Enhanced Match

$1 for $1 up to 4%

Non-Elective Contribution

3% (or more) of compensation regardless of employee deferrals

These pre-tax employer contributions are immediately 100% vested into the employee’s account. The employer can then decide whether to fund these contributions every pay period or choose a one-time end-of-year contribution.

The Second Question is Usually; “Do I have to give this benefit to all my employees?”

The answer is no. You can create eligibility, which can exclude new employees, part-time employees (those who work less than 1,000 hours a year) and young employees. The maximum eligibility is one year of service, with at least 1000 hours, and the employee must be at least 21 years of age. You can customize 401(k) plan eligibility requirements, with anything below that as well.

The Third Question I Get is Usually, “How much is this going to cost me?”

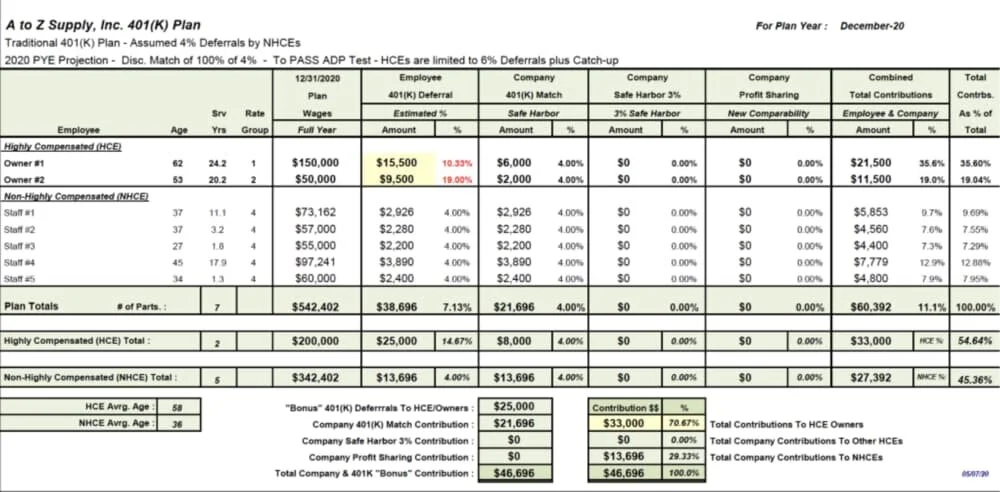

Most business owners — and their accountants — want to know what the bottom line is. For the Safe Harbor Match, you need to calculate the minimum employer contribution, which is 4% of every eligible employee’s salary. Below is an example of a table that our team of experts will create for you without charge. It will easily show you the “bottom line” of how much a Safe Harbor 401(k) plan could cost.

With this sample illustration, we show you how much each Safe Harbor option would cost your business. If you are worried about costs to the business, consider choosing a low-cost 401(k) provider that will minimize administrative costs, which makes the employer contribution seem more affordable.

401(k) Safe Harbor Rules

Important Deadlines to Remember When Starting a Safe Harbor 401(k) Plan :

Startup Plans:

Agreements received by LT Trust: September 15th, 2020

Plan Documents created and signed: September 30th, 2020

October 1st, 2020: Safe Harbor Match 401(k) Plan has started, which means your business is exempt from nondiscrimination testing for 2020

December 1st, 2020: Safe Harbor Nonelective 401(k) Plan has started, meaning that your business is exempt from nondiscrimination testing for 2020 (3% Safe Harbor contribution will be based on full year compensation)

Existing Plans:

By or before November 30th, 2020: Submit a request for a Safe Harbor Provision to your 401(k) plan for the next year

30-day notice sent to employees: December 2nd, 2020 (Only Safe Harbor Match)

Safe Harbor provisions in effect, your business is exempt from nondiscrimination testing: January 1st, 2020

Let’s circle back to why so many small businesses choose a Safe Harbor 401(k) Plan in the first place.

Key employees want to maximize their contributions and avoid testing.

A common failed test in a small business 401(k) is the Top-Heavy test.

It is more common than not for there to be a “top heavy” problem if the plan does not go Safe Harbor. This means that 60% or more of the assets in the plan are owned by key employees, resulting in a possible 3% contribution through the date of the correction.

Notable Recent Change: The SECURE Act, passed in 2019, now allows existing 401(k) plans to opt into a Safe Harbor provision mid-year with a non-elective option. The time of year that a plan elects to become a Safe Harbor plan will dictate what non-elective percentage need to be contributed to all participants.

Over 80% of LT Trust clients go Safe Harbor for a reason.

It will allow key employees to contribute the maximum contribution, receive additional savings from your company employer contributions and avoid any headaches that come from IRS non-discrimination testing.

Please feel free to meet with me to discuss questions about whether or not a safe harbor plan is right for your business!